Pitfalls in the ECB plans. Fundamental analysis for 26.08.2014

26.08.2014

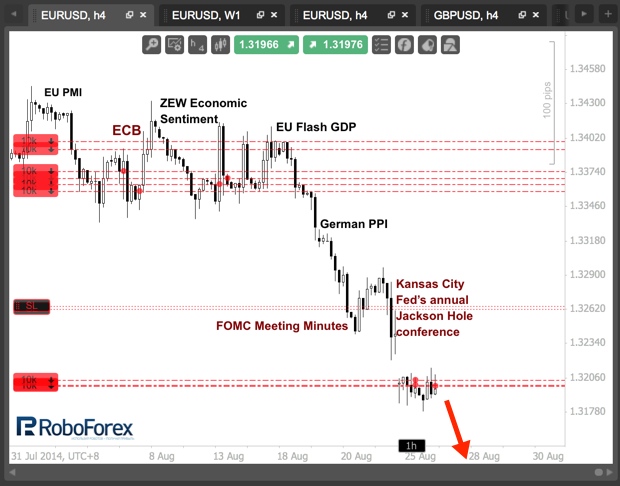

Mario Draghi’s Friday’s speech in Kansas City marked a significant shift in emphasis in the policy of the ECB. However, over the years of the monetary union the Europeans have taken on so many restrictive measures that the practical realization of all that Draghi said would be extremely difficult. In fact, he shifted the responsibility for low inflation in the national government, calling the last to think about the growth of government spending.

The fact is that as soon as there was a question about the need to tighten the belt, the European capitals went about it in the simplest way - they mercilessly closed long-term investment projects, which could have served as a basis for future growth. The logic here is more than clear as for the ordinary voter a set of social benefits is far more important. And now Draghi strongly suggests that governments begin to invest in infrastructure.

On the one hand it is a shoulder to the regulator in the fight with low inflation, and on the other – it will provide additional support for more sustainable growth in the euro zone. And here is the hitch - in the midst of crisis to somehow reassure investors, a Stability and Growth Pact was signed, which very clearly outlines the obligations of the euro zone countries to reduce their deficit and public debt levels. The European Commission was assigned to give out fines to the violators.

This is why, for example in Paris, they can not just pick up and despite quite a formal agreement with Brussels, ignore the demands to bring the budget deficit to 3% of the normal level of GDP, since then they can be fined by 0.1% of GDP. Recent comments by the Commission officials also indicate that there they do not share the enthusiasm of national governments in relation to a possible increase in costs.

For the ECB it will not be easy to implement and the asset purchase program, if the decision to launch it will still happen. The ECB are significantly limited in the spectrum of choice of financial instruments, as its mandate directly prohibits the financing of national governments, and the idea with common Eurobonds in only an idea. Consequently, the act will go through corporate bonds and credit portfolios, which is unusual for QE.

The most important achievement, which the journalists credited Mario Draghi with, is the significant depreciation of the euro. Previously, exporters regularly complained about the euro complicating their lives. On the other hand, if it were not for the delicate probing of the theme of an earlier rate hike by the Fed, the euro would have to trade at the same level as the perception of risk, and this is clearly seen in the bond market, is now somewhat distorted. In the meantime, I keep the sales positions, and I moved the stops.

RoboForex Analytical Department

The fact is that as soon as there was a question about the need to tighten the belt, the European capitals went about it in the simplest way - they mercilessly closed long-term investment projects, which could have served as a basis for future growth. The logic here is more than clear as for the ordinary voter a set of social benefits is far more important. And now Draghi strongly suggests that governments begin to invest in infrastructure.

On the one hand it is a shoulder to the regulator in the fight with low inflation, and on the other – it will provide additional support for more sustainable growth in the euro zone. And here is the hitch - in the midst of crisis to somehow reassure investors, a Stability and Growth Pact was signed, which very clearly outlines the obligations of the euro zone countries to reduce their deficit and public debt levels. The European Commission was assigned to give out fines to the violators.

This is why, for example in Paris, they can not just pick up and despite quite a formal agreement with Brussels, ignore the demands to bring the budget deficit to 3% of the normal level of GDP, since then they can be fined by 0.1% of GDP. Recent comments by the Commission officials also indicate that there they do not share the enthusiasm of national governments in relation to a possible increase in costs.

For the ECB it will not be easy to implement and the asset purchase program, if the decision to launch it will still happen. The ECB are significantly limited in the spectrum of choice of financial instruments, as its mandate directly prohibits the financing of national governments, and the idea with common Eurobonds in only an idea. Consequently, the act will go through corporate bonds and credit portfolios, which is unusual for QE.

The most important achievement, which the journalists credited Mario Draghi with, is the significant depreciation of the euro. Previously, exporters regularly complained about the euro complicating their lives. On the other hand, if it were not for the delicate probing of the theme of an earlier rate hike by the Fed, the euro would have to trade at the same level as the perception of risk, and this is clearly seen in the bond market, is now somewhat distorted. In the meantime, I keep the sales positions, and I moved the stops.

RoboForex Analytical Department

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.